This is a bit of a technical, if not tedious, read (I had to read it twice to get it), but this piece explains my concerns about the current state of the U.S. economy; although things may look good on the surface, the fundamentals are weak. We are under an illusion of prosperity, but the underlying factors say otherwise. As such, a financial reset has to occur. The question is not if, but when. No one knows the answer to this.

Why is studying economics important? Because it affects everything in your life—what you will and will not be able to do.

Yes, as believers in Yeshua, we have faith that Elohim is bigger than all of this, and he is, and that we will help us in times of trouble. But our faith in him alone without some corresponding action on our part will not carry us through the hard times that are coming on this world prior to Yeshua’s return. We still have to prepare ourselves spiritually (most importantly) and physically, as much as possible.

Having said this, I hope you will take time to read this article.

From https://www.zerohedge.com/news/2018-01-13/strange-case-falling-dollar-and-what-it-means-gold

The Strange Case Of The Falling Dollar – And What It Means For Gold

Authored by Alt-Market’s Brandon Smith via Birch Gold Group,

Trillions of dollars in uncontrolled central bank stimulus and years of artificially low interest rates have poisoned every aspect of our financial system. Nothing functions as it used to. In fact, many markets actually move in the exact opposite manner as they did before the debt crisis began in 2008. The most obvious example has been stocks, which have enjoyed the most historic bull market ever despite all fundamental data being contrary to a healthy economy.

With a so far endless supply of cheap fiat from the Federal Reserve (among other central banks), as well as near zero interest overnight loans, everyone in the economic world was wondering where all the cash was flowing to. It certainly wasn’t going into the pockets of the average citizen. Instead, we find that the real benefactors of central bank support has been the already mega-rich as the wealth gap widens beyond all reason. Furthermore, it is clear that central bank stimulus is the primary culprit behind the magical equities rally that SEEMS to be invincible.

To illustrate this correlation, one can compare the rise of the Fed’s balance sheet to the rise of the S&P 500 and see they match up almost exactly. Coincidence? I think not…

Another strangely behaving market factor that has gone mostly unnoticed has been the Dollar index (DXY). Beginning after the global financial crisis in 2008, the dollar’s value in reference to other foreign currencies initially moved in a rather predictable manner; collapsing in the face of unprecedented bailout and stimulus programs by the Fed, which required unlimited fiat creation from thin air. Naturally, commodities responded to fill the void in wealth protection and exploded in price. Oil markets in particular, which are priced only in the US dollar (something that is quickly changing today), nearly quadrupled. Gold witnessed a historic run, edging toward $2,000.

In the past few years, central banks have initiated a coordinated tightening policy, first by tapering QE, then raising interest rates, and now by decreasing their balance sheets. I would note that while oil and many other commodities plummeted in relative value to the dollar after tightening measures, gold has actually maintained a strong market presence, and has remained one of the best performing investments in recent years.

Something rather odd, however, has been happening with the dollar…

Normally, Fed tightening policies should cause an ever-increasing boost to the dollar index. Instead, the dollar is facing a swift plunge not seen since 2003.

What is going on here? Well, there are a number of factors at play.

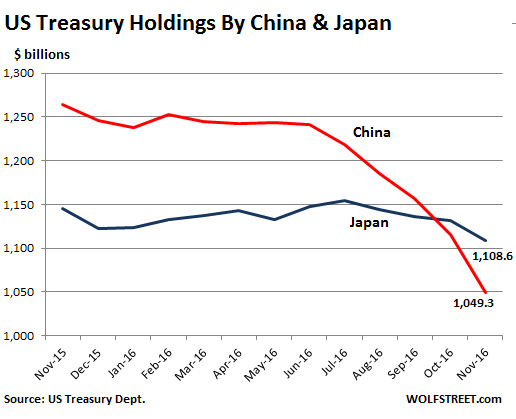

First, we have a growing international sentiment against US treasury bonds (debt), which may be affecting overall demand for the dollar, and in turn, dollar value. For example, one can see a relatively steady decline in US treasury holdings by Japan and China over the course of 2016, with China being the most aggressive in its move away from US debt:

We also have a subtle, yet increasing, international appetite for an alternative world reserve currency. The dollar has enjoyed decades of protection from the effects of fiat printing as the world reserve, but numerous countries including Russia, China, and Saudi Arabia are moving to bilateral trade agreements which cut out the US dollar as a mechanism. This will eventually trigger an avalanche of dollars flooding into the US from overseas, as they are no longer needed to execute cross-border trade. And, in turn the dollar will continue to fall in relative value to other currencies.

There is also the issue of coordinated fiscal tightening by central banks around the world, with the ECB and even Japan moving to cut off stimulus measures and QE. What this means is, other currencies will now be appreciating in terms of Forex market value against the dollar, and in turn, the dollar index will decline further. Unless the Federal Reserve acts more aggressively in its interest rate hikes, the dollar’s decline will be brutal.

Finally, we also have the issue of nearly a decade of Fed stimulus that has gone without audit (except for the limited TARP audit, which shows tens of trillions in money/debt creation). We truly have no idea how much fiat was actually created by the Fed – but we can guess that it was a massive sum according to the seemingly endless rise in equities from a point of near total breakdown, funded by quantitative easing and stock buybacks. You cannot conjure a market rebound merely with debt. Eventually, that currency creation and the consequences will have to set a foot down somewhere, and it is possible that we are witnessing the results first in the dollar, as well as the Treasury yield curve, which is now flattening faster than it did just before the stock market crash in 2008.

A flat yield curve is generally a portent of economic recession.

I believe that this is just the beginning of troubles for the dollar and for US bonds. Which raises the question, how will the Fed react to a dollar market that is so far completely ignoring their tightening policies?

Here is where things get interesting.

Throughout 2017, I warned that the Fed would continue to raise interest rates (despite many people arguing to the contrary) and would eventually find an excuse to increase rates much faster than previously stated in their dot plots. I based this prediction on the fact that the Fed is clearly moving to pop the enormous fiscal bubble it has engineered since 2008, and that they plan do this while Donald Trump is in office (whether or not Trump is aware of this plan is hard to say). Trump has already taken credit on several occasions for the epic stock rally, and thus, when the plug is pulled on equities life support, who do you think will get the blame? Definitely not the banking elites who inflated the bubble in the first place.

Even the mainstream financial media has admitted at times that Trump will “regret” his campaign demands that the Fed hike rates and stop pumping up stock markets, as he will be inheriting a fiscal punch in the gut.

The Fed, as well as the mainstream, have also planted the notion that the Fed “will be forced” to raise interest rates faster if the Trump Administration pursues its plans for Hoover-style infrastructure development.

But, on top of this, the “problem” of the falling dollar also introduces a whole new rationale for speedy interest rate hikes. I believe that soon after Janet Yellen leaves as Fed chair and Jerome Powell transitions in, the Fed will begin an exponential increase in rates and will speed up their balance sheet reductions. And, they will blame the unusual decline in the dollar index as well as falling Treasury demand as the cause for more extreme action.

Powell has already backed “gradual rate hikes” in 2018, and, a few members of the Fed expressed a need for “faster hikes” in the minutes of the last meeting in December. I predict this sentiment will expand under Powell.

A small number of Wall Street economists are also warning of more rate hikes in 2018, and that this could cause considerable shock to the virtual stock rally in play right now.

That might be the Fed’s plan. The central bankers need a scapegoat for the eventual bursting of the market bubble that they have produced. Why not simply allow that bubble to finally implode in the near term, blaming the Trump administration and, by extension, all the conservatives that supported him? To do this, the Fed needs an excuse to hike rates swiftly; and they now have that excuse with the dollar dropping like a stone (among other reasons).

But how will this affect gold?

So far, gold has actually spiked along with Fed rate increases, which might seem counter intuitive, but so is the dollar falling along with rate increases.

I do think that there will be an initial and marginal drop in gold prices if the Fed increases the frequency of rate hakes. That said, eventually reality will set into stock markets that the party is over, the punch bowl is being taken away, and Trump’s tax reform will not be enough to offset the loss of access to trillions in cheap fiat dollars from the central bank.

Once stocks begin to collapse in the wake of Fed hikes and balance sheet reductions (and they will), and uncertainty in the fate of the dollar swells, gold will bounce back stronger than ever. In the meantime, I would treat any drop in precious metals as a major buying opportunity. Gold is one of the few assets that always does well during times of crisis.